EU Preserves Impact Materiality—and the Soul of Sustainable Reporting

May 13, 2026

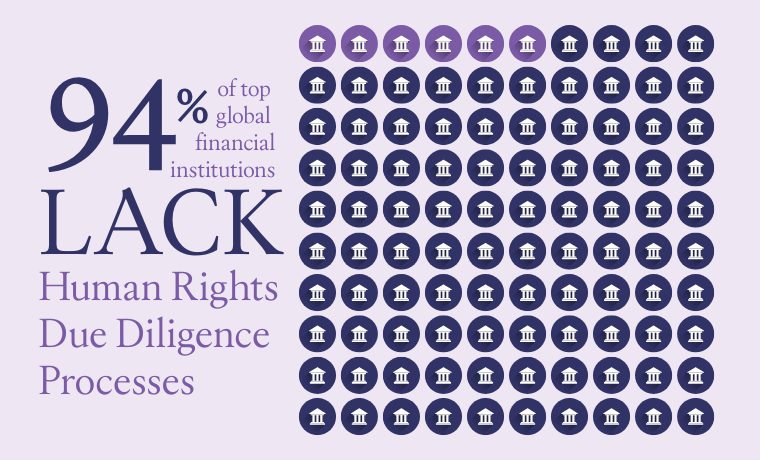

On May 6, the EU defied expectations and preserved the duty of the world’s biggest companies to disclose issues that impact the environment or society, even if they are financially immaterial. With this update of the European Sustainability Reporting Standards (ESRS), Europe’s corporate sustainability regime is now final enough to take stock. Despite significantly weakening a once-bold system of human rights regulation, Brussels has kept just enough of its essence to make the experiment worthwhile.

Sustainable regulation should not focus on financial materiality, because financially material costs are definitionally borne by shareholders, and firms are already incentivized to address them. Sustainable regulation is needed precisely where the costs of a firm’s actions are externalized and borne by the outside world, because the firm is not properly held accountable by existing legal or market pressures. The root problem is that firms often damage society without hurting shareholders. Sometimes antisocial behavior is profitable, legal, and scandal-free. More often, it’s so profitable that a firm will accept a modicum of bad publicity and legal liability, while maneuvering to minimize both.

The disclosure of actions that negatively impact the world enables regulators, or values-driven private actors, to discipline firms to internalize costs that they would otherwise impose on society. This is the idea behind sustainable reporting, investing, stewardship, and due diligence. And that is why it matters that the EU is standing by impact materiality.

The February amendments that preceded this update significantly narrowed the regime’s scope. For starters, between 70 and 90 percent of previously covered firms are now exempt. Firms that remain covered will need only to do due diligence on direct suppliers, not their full value chains. They will no longer be obliged to meet sector-specific reporting standards. Their due diligence reports will never be audited to the same level of assurance as their financial statements. And EU states are free to make their judicial liability systems as weak as they like.

The newly updated reporting standards, issued by the European Financial Reporting Advisory Group (EFRAG), retreat further on a few fronts. For instance, human rights violations will need to be reported only if they are “substantiated.” Human rights complaints will need to be reported only if they are “ongoing.” These qualifications risk creating reporting loopholes that allow companies to disclose only what has already been publicly established, rather than surfacing emerging concerns. We urge EFRAG to reconsider these points.

Yet the May 6 update is most notable for resisting the pressure from big business to prioritize financial materiality in sustainability reporting. According to Responsible Investor, the EU had considered aligning the ESRS with the standards of the International Sustainability Standards Board (ISSB), which addresses human rights concerns only if they pinch shareholders. ISSB chair Emmanuel Faber, the leading advocate for the proposed change, wished for impact materiality to be presented in a way that did not “obscure” or distract from financial materiality, arguing that financial materiality “is the most urgent lever, because it will move capital allocations.”

Critics, including Frederic Ducoulombier of EDHEC Business School, rightly warned that aligning the two sets of standards would have subordinated impact materiality to financial materiality—a structural shift that would have hollowed out the ESRS’s core purpose.

In contrast to the ISSB standards, the ESRS forces firms to disclose problems that impact the world, even if shareholders are unharmed. The EU’s decision to hold the line reflects a well-founded judgment that financial and impact materiality are not interchangeable. This Center has long taken the position that sustainable reporting must focus on how business harms the world, not on how business is harmed by sustainability scandals.

According to the SOMO CSDDD Datahub, the European due diligence directive in its current form will capture 965 corporate groups in the EU, 182 in the US, and 300 in the rest of the world, as well as their direct suppliers. This universe could have been much larger. But it still captures the behemoths of the global economy, and submits them to a regime of enforceable human rights law with administrative penalties up to 3% of global revenues. Most importantly, it creates a rare legal system where large multinationals will be forced to report the harms that they inflict on society even where shareholders may benefit. Moving forward, investors and civil society should push EU regulators to hold firms meaningfully accountable when they fail to remediate those harms, and push EU states to create toothsome systems of judicial liability.

Values-Based Investing

Values-Based InvestingRelated

See all